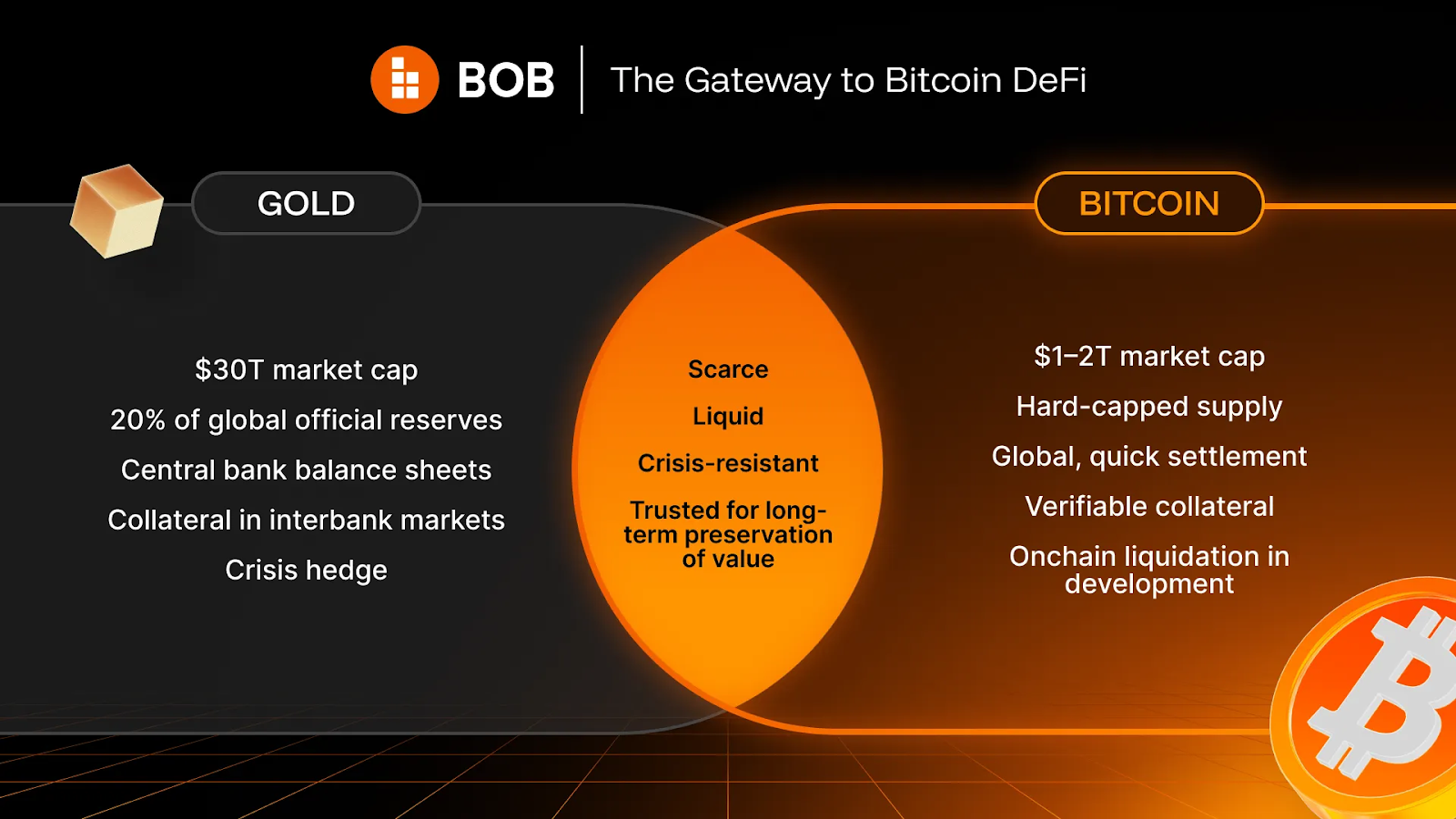

Bitcoin is the best collateral ever created. Verifiable, easily transferable globally, divisible and liquid 24/7. Nothing else comes close. Yet we are still early, and only a fraction of Bitcoin is being put to work in both traditional and non-traditional markets. Approximately 2% of Bitcoin's ~$1.4 trillion market cap is currently deployed across Bitcoin-native protocols and sidesystems, while only ~0.3% of BTC is in true native BTCFi. Much of the remaining 98% sits idle, signalling massive potential when stacked up against gold, silver and other precious metals.

Due to its superior attributes, some leading macro analysts believe that Bitcoin surpassing gold's $30 trillion market cap is a question of when, not if. Should Bitcoin reach that level, and 30% of that value is used as productive collateral (matching ETH's current onchain participation), that's a $6 trillion market waiting to be unlocked. Combined with limited confidence in banks as institutions, the case for Bitcoin-native financial infrastructure has never been stronger.

BOB is building that infrastructure: one banking stack for spending, saving, earning, and borrowing - all on Bitcoin rails. Exactly what neobanks did for fiat, but without the legacy system underneath. We've spent years building the foundation for this moment. Now, we're going all in.

One asset. Many trillion-dollar markets

To understand the scale of this, consider some of the traditional market opportunities that Bitcoin-powered banking rails could tap into:

[Image data sources: McKinsey Global Banking Annual Review 2025 (Global Consumer Deposits), ICI (Money Market Funds), World Bank (SME Finance Gap), ADB Global Trade Finance Gap Survey 2025 (Trade Finance Gap), EMF Hypostat 2025 & PBOC via Reuters (Mortgages)]

Take consumer deposits alone. Approximately $23 trillion of the $70 trillion in consumer deposits globally sits in checking accounts with near-zero rates, while banks lend it out at multiples, pocketing the spread. Savers absorb inflation risk while institutions capture the upside. The same story plays out across mortgages and trade finance - high fees, slow settlement, geographic restrictions, opaque terms.

The point is that infrastructure serving these markets hasn't changed in decades. But Bitcoin-backed banking can change that through transparent rates, programmatic terms, and yield that flows back to the holder - not the middleman. And the exciting thing is that there are already early signs which indicate a growing interest in banking products that revolve around Bitcoin.

In crypto alone, collateralised lending (much of which backed by BTC) reached a new all-time high of $73 billion in Q3 2025. At the same time, native Bitcoin DeFi grew to ~$9 billion TVL in late-2025.

When it comes to mainstream interest, major U.S. lender Newrez recently announced that it now accepts BTC for mortgage qualification, Enness Global reports a 214% rise in crypto-backed loan inquiries, and crypto card volumes have grown from $100 million to $1.5 billion per month in just two years.

So what's standing in the way? It’s not Bitcoin. It's a lack of banking infrastructure that holders and non-holders can trust, benefit from, and access from one place as easily as any app on their phone.

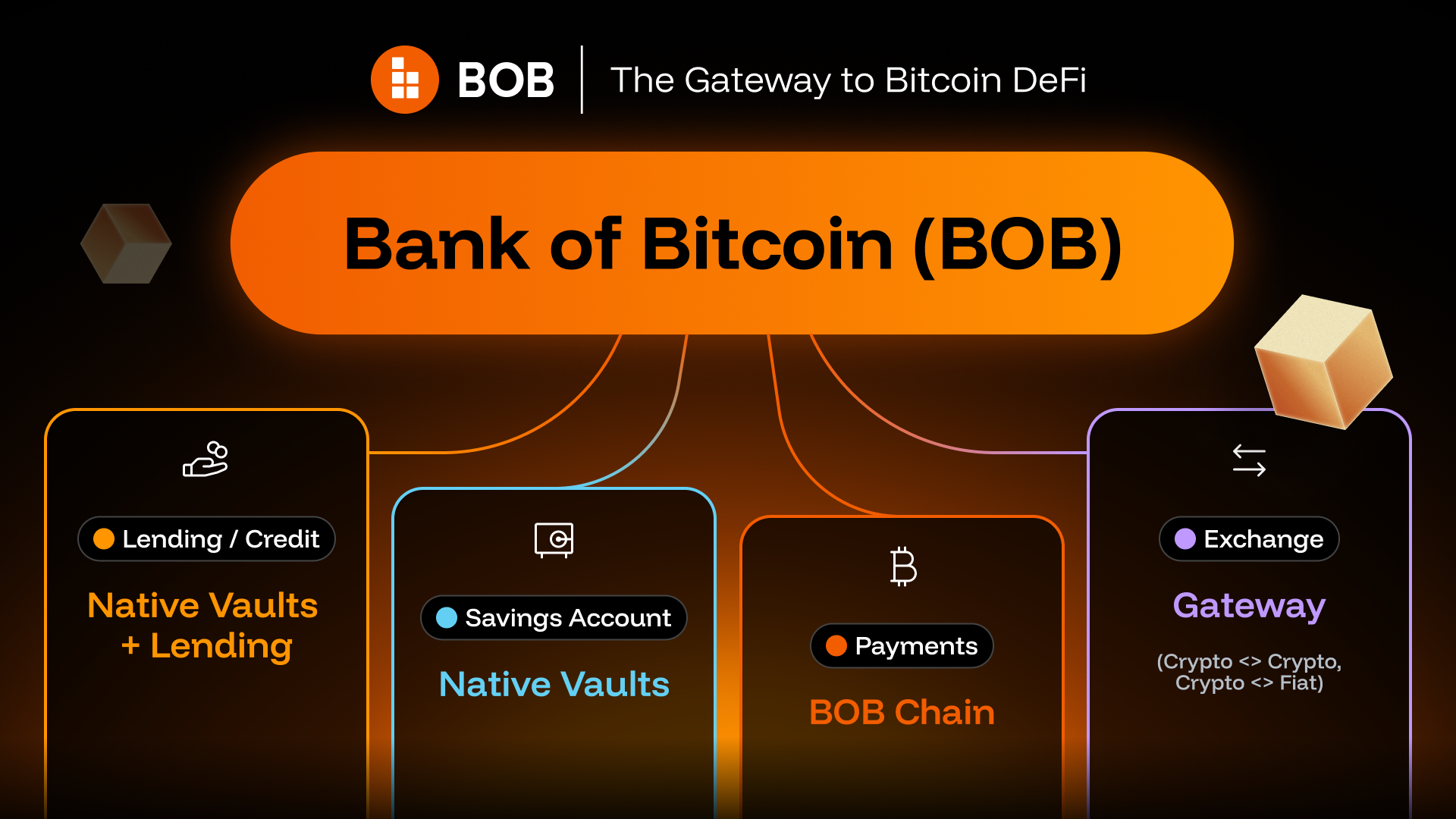

Your money on Bitcoin rails

Everything BOB is working on will bring us closer to the Bank of Bitcoin:

- BOB Gateway - Your exchange. Swap native BTC to any asset on any chain, or crypto to fiat. One click only.

- Native Vaults - Your savings account. Earn yield on your BTC. Your exact coins stay on Bitcoin.

- Lending - Your credit line. Borrow stables against your BTC. Transparent terms, liquidations settled on Bitcoin.

- Payments - Your everyday spending. Pay for goods and services using your Bitcoin, even without needing to sell it.

This will be a significant improvement on what already exists. Centralized exchanges hold your keys, current lending methods use wrapped BTC backed by custodians or multisig bridges, and 40+ wrapper variants across dozens of chains make the experience fragmented and confusing. BOB’s native Bitcoin banking infrastructure will remove these tradeoffs. Now picture what this could mean in practice…

- A freelancer in Buenos Aires gets paid in BTC and borrows stables against it to cover rent. Her coins stay secured on Bitcoin. When she repays, she gets the exact same sats back.

- A retiree in Lisbon earns transparent yield on his savings and sees exactly where returns come from, no bank taking the spread.

- A founder in Singapore swaps through Gateway at 2am to make payroll across three currencies. No exchange account, no market hours, funds arrive in minutes.

- A long-term holder in Austin covers everyday expenses using yield alone. Principal untouched. BTC never sold.

Different people. Different continents. Different needs. All using the same Bank of Bitcoin rails. Not wrapped tokens on a third-party chain. Not custodial IOUs from a lender that might not survive the next cycle. Real financial products built on Bitcoin's security, open to anyone with a wallet.

If even a fraction of the trillion-dollar markets move onto these rails, the numbers get serious. Hundreds of billions in loan volume. Hundreds of billions in productive TVL. Every swap, every loan, every vault deposit generating fees. In other words, the infrastructure that captures this flow captures the value.

Three Bitcoin banking pillars powered by the BOB Hybrid Chain

The Bank of Bitcoin doesn't get built overnight. It requires a foundation, distribution, and killer financial products. That's why 2026 is the year of focus for BOB, and by concentrating our resources we will accelerate the path to making Banking on Bitcoin a reality.

It starts with three pillars:

- BOB Gateway is the onboarding and distribution layer for the Bank of Bitcoin. Native BTC swaps are the onramp, enabling deposits and DeFi deployments across 100+ chains in the future. Any wallet or fintech can plug in. Every transaction routes through BOB, generating protocol revenue.

- Native Bitcoin Vaults are the savings and lending engine. Turn idle BTC into productive collateral. Borrow stables, earn yield, and always receive your exact sats back on Bitcoin. BOB's new liquidation model enables permissionless BTC-backed stablecoin loans at scale, with BitVM able to enforce the rules trustlessly - removing the need for wrappers or custodians.

- A frictionless consumer app. Imagine being able to borrow against your BTC for everyday spending - no selling, no traditional bank required. This is just one Bitcoin banking product that will be possible once BOB builds out the stack.

As this article goes live, the team is already accelerating Gateway integrations and finalizing our design for Native vaults for launch - with work also underway on what could become one of the first native BTC consumer banking products ever built.

The $6 trillion endgame

The current financial system runs on layers of intermediaries. When money crosses a border, it passes through correspondent banks with nostro and vostro accounts, each taking a cut, each adding a day. When a loan gets made, it moves through credit bureaus, underwriters, loan officers, servicers. When a trade settles, it clears through custodians, clearinghouses, settlement banks. Every layer exists because trust has to be manufactured somewhere.

Bitcoin doesn't need those layers. Trust is built into the protocol. No long waits for final settlement. Collateral is verifiable onchain, not locked in someone else's system. Code executes the agreement. No loan officer. No five layers of intermediaries, each extracting their percentage.

What remains is protocol and user. The infrastructure flattens. A single global settlement layer replaces thousands of bilateral banking relationships. Smart contracts replace the paperwork. Self-custody replaces the custodian. The functions don't disappear. The extractive middlemen do.

That's the $6 trillion endgame. Not just better products. A different architecture entirely. One where the value that used to leak to intermediaries stays with the people who created it.

That’s what BOB is building. BOB will be the Bank of Bitcoin.

*To learn more about BOB’s Bank of Bitcoin vision, check out Alexei’s blog here.

.webp)